Philippines Yield · The Cost Stack

Philippines condo fee stack: the VAT and CGT trap.

The developer quotes a price per square metre because the price per square metre closes the sale. The number that actually leaves your account at registration is the price plus a stack of taxes and fees nobody itemised in the showroom. The Philippine stack is wider than most home markets and the obligations are split between buyer and seller by custom, not always by statute, and that split is where the trap lives. This page opens every line so you can build the spreadsheet yourself. Pillar-level context lives at the Philippines foreign-buyer reality check.

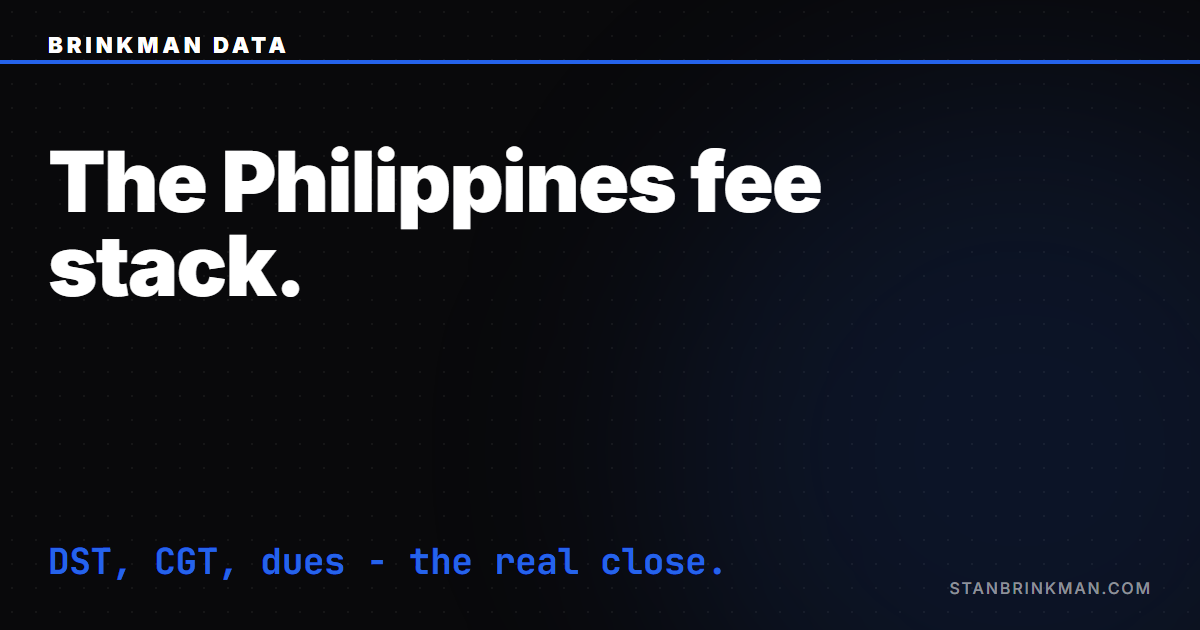

12%

VAT on new-build developer sales

6%

CGT, split decided by contract

1.5%

documentary stamp tax